If telco and communications spend is a significant part of your budget and supports how you operate as an organisation, then this post is for you.

Telecommunications, in its widest sense is a fundamental component how an organisation supports and engages with its internal and external customers. The telecommunication industry is undergoing significant change at an industry, technical, functionality and user level.

These changes have led to increased productivity, reduced costs, and improved services for businesses.

However, they also bring complexity and challenges in implementation, user adoption, and security.

Organisations must carefully plan and manage these changes to achieve the promised benefits.

We have put together this summary to help inform what best areas to concentrate on.

In today’s climate, business and IT leaders are balancing what to focus their energy and resources on. When we’re working with clients, these are some of the factors they weigh up when thinking about change to their telecommunications platforms:

Productivity: How will the much-promised Information Communication Technology (ICT) features and benefits translate into more revenue, better services, reduced costs and how long will these last over time?

Impact of change: How will users and customers react to complexity and the pace of change? How will technical changes affect the interconnectedness of systems and new capabilities

Risk and security: ICT leaders having to keep the organisation safe, while at the same time not hamstringing it from being able to work, flex, evolve and be flexible

Budgets: Budgets are always limited. How can more be done with less? What are the benefits of investing in new systems and functionality versus making legacy systems last?

This blog will help you answer these questions:

What is changing in the industry and how might this affect your organisation?

What areas offer the most promise of improving productivity?

What areas should procurement tenders focus?

Where AI is being practically implemented – is it worth it for your organisation?

In brief

How organisations are working and communicating continues to change. At the same time, the telecommunications industry is undergoing significant changes, driven by factors such as the global pandemic, the adoption of cloud-based services, and the entrance of big tech companies like Microsoft and Zoom. These changes have led to increased productivity, reduced costs, and improved services for businesses. However, they also bring complexity and challenges in implementation, user adoption, and security. Organisations must carefully plan and manage these changes to achieve the promised benefits.

We’ve summarised our key insights and reflections on how you can ensure your organisation can achieve this. This blog will help you answer these questions:

What is changing in the industry and how might this affect your organisation?

What areas offer the most promise of improving productivity?

What areas should procurement tender focus?

Where AI is being practically implemented – is it worth it for your organisation?

1. Introduction

Telecommunications, in its widest sense is a fundamental component how an organisation supports and engages with its internal and external customers. The telecommunication industry is undergoing significant change at an industry, technical, functionality and user level.

With promised potential to improve services, reduce costs and build on productivity, we’ve put together this summary based on our experience with larger businesses and corporate clients to help inform what best areas to concentrate on.

In today’s climate, business and IT leaders are balancing what to focus their energy and resources on. When we’re working with clients, these are some of the factors they weigh up when thinking about change to their telecommunications platforms:

Productivity: How will the much-promised Information Communication Technology (ICT) features and benefits translate into more revenue, better services, reduced costs and how long will these last over time?

Impact of change: How will users and customers react to complexity and the pace of change? How will technical changes affect the interconnectedness of systems and new capabilities

Risk and Security: ICT leaders having to keep the organisation safe, while at the same time not hamstringing it from being able to work, flex, evolve and be flexible

Budgets: Budgets are always limited. How can more be done with less? What are the benefits of investing in new systems and functionality versus making legacy systems last?

2. Telco definitions

For context, when we use the term telecommunications we are referring to:

Unified Communications and Collaboration applications such as Zoom and Microsoft Teams calling

Mobile voice and data, and applications, such as Voice calling, Teams, Zoom, messaging apps and social media, on these devices

Data networks that connect organisations together

Contact centre functions to manage customer interactions and experiences

Legacy services including landlines, analogue lines, PBXs, data circuits and some radio services

Suppliers, including the large telecommunications companies, ISP and Service Providers

3. What’s Changing?

Over the last 3-4 years telecommunications services have changed significantly for individuals and businesses. These changes promise genuine productivity improvements.

The drivers and enablers for these rapid changes include:

The Global Pandemic forced and legitimised the need to be able to work seamlessly from home or office and significantly accelerated the adoption. However we note, in rolling out these new services in haste, some systems were implemented in a minimum viable proposition (MVP) from a feature and training perspective

Cloud based Software as a Service and storage services

The availability of affordable fibre connections to homes and businesses, providing increased bandwidth along with more pervasive high speed mobile data

Big Tech’s entrance in the market with new communication tools, such as Microsoft Teams, and Zoom that offer new features that take advantage of increased available bandwidth. These better support new ways of working, such as remote working capability and richer collaboration from any device

Influenced by the consumer market to be always on and available, organisations are under pressure to provide services outside of traditional working hours and in ways that make it easier to service their customers.

These changes come with cost and are not without complexity. Internal IT teams must decide what to buy and who to buy from, then how to implement services. For users and customers there change and potentially disruption. To achieve promised productivity improvements, implementations must be planned, sometimes over several periods.

Using our 10 years of direct consulting experience with New Zealand organisations and a career in telecommunications, our principal consultant for Communications and Collaboration, Dave Gibbon, has led these insights on the current state of modern communications and collaboration.

We hope these observations and reflections present opportunities to improve services and save you time and cost as your organisation navigates modern telecommunications options.

4. We are in a transition

As organisations adopt modern workplace strategies, using for example Microsoft Teams or Zoom, the use of traditional telephone phone calls is decreasing. These are being replaced by digital interaction channels such as chat (for example: Teams, WhatsApp, Facebook Messenger) or video calling (for example: Zoom, Google Meet and Microsoft Teams). These reconfigured and new services tend to be more efficient and cost-effective and maybe driven by users or customers. The number of choices drives complexity for organisations as they try to figure out what systems to embrace and how do this this.

Within our clients (larger businesses, corporates and local government), Microsoft Teams is by far the most chosen platform for unified communication and collaboration.

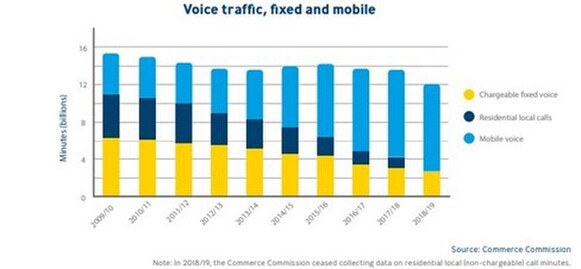

Except for contact centres and exceptional business requirements, mobile phones have become the preferred tool for voice calling. This graph from The Commerce Commission is a few years old now, but clearly shows the trend away from fixed lines, and overall, a reduction in voice calling minutes. This is a continuing trend.

While there are considerable advantages in new Unified Communication applications, the introduction of multiple suppliers, solutions and an increased level of change for uses, means there is increased complexity in selecting a solution (as there are more of them) and a greater dependence on these suppliers. The choice of applications and their implementation (including change management support) is important to achieve the promised productivity improvements.

We see some businesses implementing their new solutions in a MVP mode, that is, just enough to cover basic requirements. This reduces implementation time but may limit the productivity gains the new technology offers if additional feature sets are not added over time.

5. Cost impacts

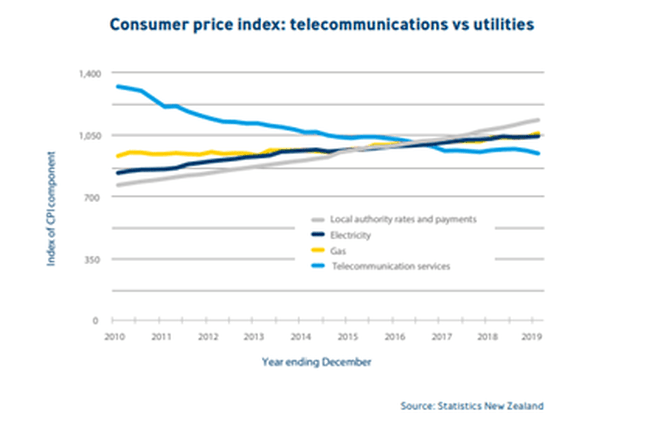

In our opinion, within the New Zealand context, the two most influential changes to affect business pricing have been telecommunications regulation the introduction of a major telco from about 2009 and an expansive fibre network, whose first phase was completed in 2019.

We have seen the effect of these influential changes in the pricing of tender response, which have shown reduced costs for business customers over a sustained period.

This can also be seen in the following graph from Statistics New Zealand showing telecommunications share of CPI (spend) relative to other utilities.

These local market changes, together with changing technology options have several important implications:

Telecommunications voice spend, has continued to fall. In our tender work with business, most companies have negotiated lower prices for current mobile services and the migration and rationalisation away from fixed services has allowed investment in newer more feature rich tools. This has typically seen an overall reduction in costs, although additional licensing costs (such as the uplift to Teams voice) for services cannot be ignored

Data pricing was the laggard in pricing change for business, but with the dominance of fibre internet connections and additional service providers, our experience of overall data costs has followed the same trend as voice, resulting in a significant reduction in cost. With the trend towards the internet for data networking, we believe pricing will stabilise at current levels

Commoditisation of services like the use of internet for connectivity, and similarities in technology and coverage across the mobile networks, means less differentiation of core services. This means customers find it easier to shift services to other providers with a corresponding downward pressure on rates

Declining revenue means telecommunications companies have responded shifting some front-line staff to call centres (our customers tell us this means there are fewer account and support staff) and branching out with related services such as security, managed services, security and general IT services

Reducing bundle pricing overages, for example uncapped calling and data, or negotiated increases in data ‘buckets’ has meant more predictable costs.

With a trend of reducing prices over an extended period we now note increases in pricing for standard business plans (as opposed to negotiated corporate plans) for fibre-based services and mobile.

While tender driven procurement processes for larger organisations and corporates shows mobile data pricing still reducing. Overall, we think telcos are signalling price increases, particularly on fixed data services.

6. Complexity has shifted

While user-function capability has increased with Unified Communication platforms, the connection to the telco networks has become simpler. The telco or carrier connection is now often a commodity service, albeit that it requires configuration within the Unified Communication aaS platform for each customer. Gone are the days where organisations need to deploy and struggle with geographically spread, analogue, ISDN and/or SIP carrier connections.

Complexity is now found where integration/interoperability is required between multiple platforms: for example, between a Unified Communication platform and a contact centre or CRM. This complexity often falls to the customer’s ICT team and their suppliers to manage and resolve.

The increased capability of the platforms cannot be ignored from a change management or end user use productivity perspective. That is, to get the most of the new platforms, to build capacity and realise productivity, change management and user training are important.

As mentioned above, where an MVP approach is adopted for implementation, it is important to plan to develop the platform to its full potential to maximise productivity.

7. What’s the impact on Telecommunication companies?

According to this 2022 report from the Boston Consulting Group (BCG) there are clear trends impacting how our telecommunications suppliers are reacting to difficult financial conditions with falling margins and rapidly changing technology requiring capital investment. We have seen these trends here in New Zealand. For example:

· Intensifying competition from hyperscalers or cloud platforms (such as Microsoft and AWS) and alternative networks such as Starlink, are delivering products and services that eat away at traditional services

· 5G is considered a core differentiator and is likely to increase in influence as demand for services that use its performance increases

· Structural separation of physical network and services has occurred and may be partly responsible for new services as telecommunication companies change: BCG calls this “telco moves to techco”. New Zealand examples are Spark’s acquisition of CCL, OneNZ’s security service and 2degrees Managed Services.

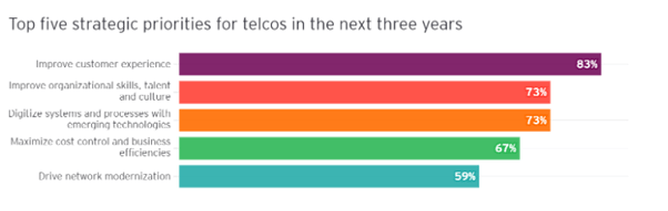

This survey of 63 leaders from worldwide telcos (including 4 or 5 from Asia Pacific) carried out for EY Global in this 2024 Are leaders ready for the telco of tomorrow? Podcast shows the top five strategic priorities for telco. The top priority is improving customer service.

What does this mean for commercial customers? Some of our clients tell us the implications of these changes are:

More and more businesses use telecommunications services provided by multiple suppliers rather than a single ‘telco’

There is less perceived differentiation of core telco services, and this means it is easier to shift suppliers

Generally new solutions are more reliable and cost effective

The range of services provided by telecommunication companies has expanded, adding to choice in the market. The exception is mobile, which is realistically limited to the three mobile carriers, especially within a competitive tender environment

New options for remote usage such as site redundancy (4/5G and Starlink) have made positive changes for office resiliency

Reduced service levels from front line staff as telcos move staff to call centres and centralise some services to save costs. Services such as timely reviews of service, new product and service or innovation discussions and management of accounts are examples. This is a complicated issue, but a common reflection from customers.

8. Focus on productivity

In a more holistic sense, the integration of communication and other business applications opens the opportunity to improve productivity by enhancing business process with a focus on customer experience, efficiency and cost savings.

These are important with the promise of improved customer experience, internal collaboration, and processing speed. That is, better or faster results. For example:

Contact centre call staff can share product documents, access customer information, and record the interaction, meaning a more effective and productive experience

Applications such as HubSpot, Microsoft Dynamics and Salesforce (CRMs) are now adding telephony, email, and messaging to directly engage with customers from within their platform. This improves access to tools and results in improved productivity and a richer and more flexible customer experience.

A general trend is to use real-time context-based information with a choice of interaction mediums to tailor the customer experience.

9. Contact centre is where AI is being trialled

While still in its infancy for many organisations, the advent of the AI bot is allowing organisations to experiment with AI as a tool to enhance customer experience and shed load from often oversubscribed contact centres.

Natural language processing and sentiment analysis tools are also emerging as tools to enhance the customer experience, improve productivity, and deliver richer analytics.

AI bots and voice recognition Interactive Voice Response (IVRs) systems are now commonplace across the market, although their widespread acceptance by the customer base is still a work in progress. This is expected to change as systems continue to improve, and this is recognised by users who will be more likely to use them.

We are seeing the use of artificial intelligence (AI) to increase productivity and efficiency.

Features such as process automation based on real time context and content in depth data analytics, and retrieval and assisted content creation.

For example, Contact/Customer Experience solutions are quickly embracing this technology to speed up interactions, manage peak call volumes and lower call wait times by filtering callers using AI based operators (BOTs) and providing information based on discussion context. The use of advanced speech analytics and recognition and sentiment analysis is being used to monitor and improve how interactions are handled.

10 Networking - emphasis on secure and flexible connectivity

Secure connectivity has become critical and underpins all the above as more staff work from anywhere, from any device, and require access to applications in the cloud. For some, access to legacy tools still within a private cloud is also a consideration.

The legacy on premise location-based perimeter firewall has given way to cloud centric security tools that reflect the requirement to securely access data in the cloud regardless of where staff are accessing it from. The new focus on software-based security tools, including the use of AI will allow organisations to stay on top of emerging threats and better predict potential vulnerabilities.

These are important topics and must be considered early on in change proposals.

In conclusion

Communication plays a strategic role for most organisations and consumes a significant amount of budget. We are seeing ongoing changes in the telco landscape – much of which is positive for organisations, but which can also lead to increased complexity, poor service and rising costs.

This post aims to help you understand and navigate the changes in a way that is right for your organisation, ensuring you get the value from your investments.

if you’ve got questions or comments, don’t hesitate to contact Dave Gibbon or Kerry McFetridge.

Some of the areas we can help include:

Procurement of telco services – independent advice to ensure you have the right telco partner and the best services for your organisation

Telco Audit – reduce and consolidate your telco spend, saving you $$$s

Free Telco Scorecard - not sure where to start? A few questions gives you a tailored action plan for better services, improved technologies AND save thousands of dollars on your telco bill